Ease in filing of

income tax returns as well as strengthening the online grievance redressal mechanism for taxpayers are two key demands made by the common man with regard to tax administrative changes. India’s tax laws are rather complex and for simple tax calculations too one has to do two computations to figure out which method of taxation works better.

Tax return forms require various details for all kinds of investments, capital gains, bank interest calculations, dividend earned etc. For example, for capital gains and dividends, you have to give quarter-wise details to compute interest liability as well as transaction wise details of shares sold on stock markets for computation of capital gains. For bank interest, you have to calculate your yearly interest based on the quarterly interest received from the bank. Moreover, the returns forms change each year, making the task of filing returns rather tedious and confusing.

While various taxpayer friendly initiatives have been launched by the government to bolster the transparency of financial transactions in the country such as

E-Sahyog ( a paperless mechanism whereby the income tax (IT) department notifies assesses electronically), e-verification of ITR to shorten the processing time and issuance of refunds, Income Disclosure Scheme (IDS), increase in PAN cards issued, and TDS SMS alerts, , a lot needs to be done to ensure the entire system remains seamless in administration, information is readily available, and facilities are accessible to all, according to Dezan Shira & Associates.

Here are a few ways Finance Minister Nirmala Sitharaman can make life easier for income tax payers in India:1. Keep just one tax regime as opposed to an old and new one: A

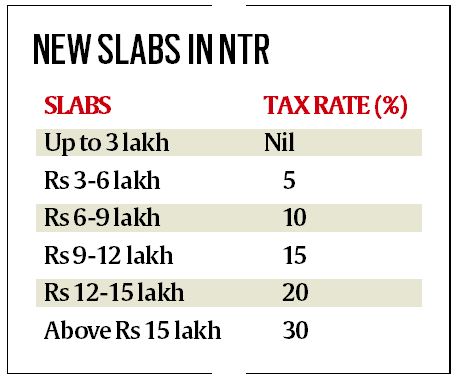

new tax regime was introduced in the 2020-2021 budget to offer taxpayers a simplified tax regime with more graded slabs that offered benefits to those not opting for exemptions and deductions but data from tax service provider Clear shows only 10% of taxpayers who utilized its portal for tax filing opted for the new regime. Unlike the new system, the

old tax regime offers various exemptions and benefits, and it appears that a considerable percentage of individual taxpayers continue to prefer that.

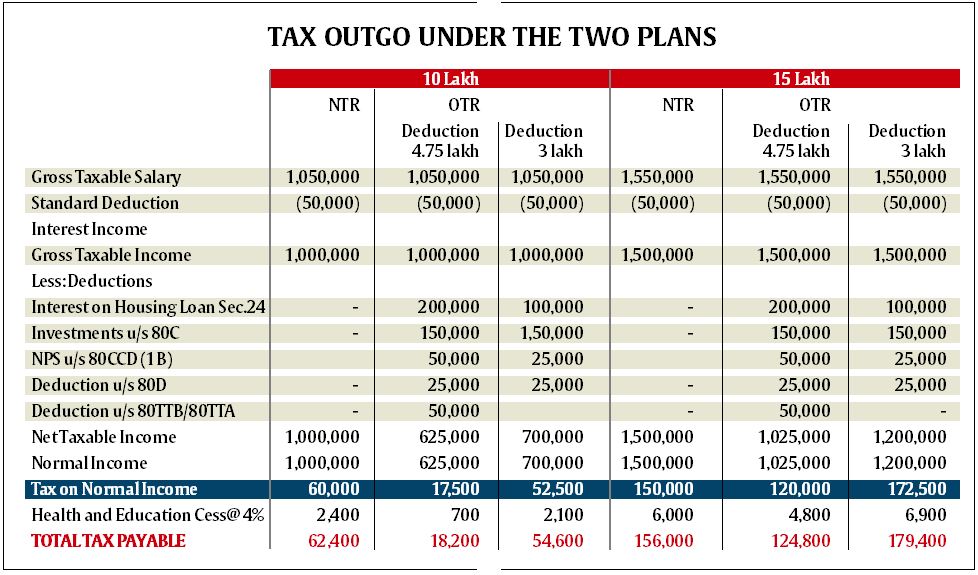

“Individuals find the old regime is better because the various tax deductions and exemptions can effectively reduce the tax on a CTC of Rs 10 lakh, which is unlikely in case under the new regime. Individuals with an income bracket of up to 5 lacs and between Rs 5-10 lakh with lower deductions claims will benefit from the new regime. But on the other hand, individuals under a higher income tax bracket above Rs 10 lakh of income per annum will end up paying more tax under the new tax regime, else could have been benefitted more from the existing regime by making tax-saving investments,” says CA Ruchika Bhagat, MD, Neeraj Bhagat & Co.

“From a tax payer’s perspective, two income tax regimes are confusing and the existing income tax slabs must be revised. In taxation, there should be no confusion or uncertainty. There is a compelling justification for further individual income tax rate rationalisation,” said Bhagat. Hence, the government should consider unifying and retaining only one simplified regime going forward.

For individual taxpayers it is becoming tough to understand the pros and cons of each regime. In fact most of the individuals are struggling to find out which one would be more beneficial in one’s specific case. “Various exemptions and deductions are available under the provisions and the composition of these tax benefits widely differ from person to person. Hence, a comparative statement cannot be standardised as to depict which regime is more beneficial and this is demotivating the individuals regarding compliance of filing ITR. The government should standardise the rates and simplify the law and process to encourage more and more individuals for the compliance. In case the government wants to keep motivating individuals for savings and investments, instead of allowing as deduction from total income, the earnings from such investments can be made exempted and a simplified one single regime can be implemented so that lower current tax rate and reduced burden of tax in future on invested money shall motivate the individuals for compliance,” recommends Vinita Krishnan, Partner, Khaitan & Co.

Also, since individual taxpayers have an option to opt in and out of the new scheme, it unnecessarily results in a compliance burden for companies, for they will have to maintain requisite data sets of employees choosing the new regime, those sticking with the old regime, and those switching between the two.

Clear’s Archit Gupta recommends only one tax regime with a lower tax burden and one way to achieve this is to increment standard deduction annually based on inflation. He also recommends removing redundant exemptions such as children’s education allowance or hostel expenditure allowance and instead allow deductions for those who work from home.

2. Make the first appellate / dispute resolution mechanism provided under the Act more effective: Assessment and appeal processes have seen major transformation in the recent years. While these initiatives have eliminated the need for personal interface between tax officers and assessees, there have been teething problems in implementation. Further finetuning of these processes by introduction of necessary legislative changes and clarification will help the taxpayers reap the benefit of these reforms fully, said S.Vasudevan, Executive Partner, Lakshmikumaran & Sridharan Attorneys.

“The dispute resolution appellate is not in reality independent, in the sense that they report to CBDT (under the Ministry of Finance), the same administrative body which appraises them for

tax collection. If the officers posted under first appellate / dispute resolution mechanism are shifted under the Ministry of Law and Justice while being posted as appellate / dispute resolution officers, the result will be far more effective. We have proof of that in the functioning of the highly respected Income-tax Appellate Tribunal,” said Nishant Thakkar, Partner, Lumiere Law Partners.

Secondly, the current first appellate mechanism does not give any priority to individuals and in particular senior citizens and hence their appeals take very long to be heard and disposed of. “The priority being suggested is a well-recognised classification for e.g. the High Courts have a separate list for all senior citizen litigation, the Income-tax Appellate Tribunal has a separate Bench for small matters (Single Member Matters) etc. If such a priority is made available at the first appellate stage, it would be of great help to individuals and in particular senior citizens,” added Thakkar.

3 Simply the online tax return forms: The FM should make a genuine effort to simplify online tax return forms and make confirmations and disclosures optional for individual taxpayers. “Ease of Tax Filing is getting worse and rates of people not filing returns is going higher. “Currently apart from filling income tax return (‘ITR’), taxpayer is also required to make various other compliances (e.g. to file form 10IE for opting new tax regime, form 67 for claiming a foreign tax credit, Form 10BA for claiming deduction u/s 80GG, etc.). The information which is to be furnished in these forms are otherwise required to be furnished in the ITR and creates multiple compliance requirements. Government should eliminate such multiple compliances and make the ITR form as a single document for all such compliances,” said Ashok Shah-Partner, NA Shah Associates.

4. Integration: Interest that gets accumulated in your savings bank account must be declared in your tax return under income from other sources. Interest from both fixed deposit and recurring deposits is taxable while interest from savings bank account and post office deposits are tax-deductible to a certain extent. But they are shown under income from other sources, explains Clear. But more often than not, taxpayers, because of lack of awareness, forget to put the fixed deposit interest/ Saving account interest in the ITR. “If, this can be integrated with the Annual Information System and if the data can be pulled automatically, it will reduce the compliance burden and will also make sure that there is a high degree of tax compliance,” said Gaurav Garg, Head of Research at CapitalVia Global Research.

Many taxpayers lament that the compliance burden has increased with two forms to be reviewed, Form 26AS and AIS. ” The finance minister can consider incorporating the details of LIC premium paid, Public Provident Fund, home loan interest and principal payment etc in Form no 26AS/AIS. With this, the small individuals and businessmen will have easy access to all the deductions/ exemptions in Form no 26AS/AIS,” said Shah.

Form 26AS and AIS should be merged and consolidated into one, recommends Clear’s Gupta.

Moreover, by introducing the new TDS and TCS provisions in relation to sale and purchase of goods, the government has unnecessarily created new compliance burdens for transactions which were already covered under other reporting mechanism such as in GST billing. Thus, the government should consider withdrawing these provisions, said Vinita Krishna.

5 Introduction of Inflation-indexed Basic Exemption Limit: Currently, we have a system where exemption limits are set every year — or not changed at all. Whether it is the basic tax-free income limit or the limits for Section 80 C deductions, inflation erodes it each year. “An index-linked system of tax exemptions and deductions will allow citizens to be spared higher taxes resulting only from inflation,” said Anand Chatrath, Managing Partner, B M Chatrath& Co LLP. He also recommends that the divergence between corporate and personal income tax rates be brought down through rationalisation of surcharge and reduction of taxes at the top end of the bracket. “Or else, individuals with high tax rates over 30 percent will shift incomes to corporates owned by them. A five-year plan to converge personal tax rates towards corporate ones (now in the 15-25 percent range) should be announced in the budget,” said Chatrath.