Union Budget 2023 may look to tweak the alternate income tax regime in order to make it more attractive for individual taxpayers, says a news report. The Modi government is mulling the possibility of raising the tax free

income tax slab from Rs 2.5 lakh at present to Rs 5 lakh under the new income tax regime, the report said.

How will this benefit salaried tax payers? Will a change in income tax slabs for FY 2023-24 under Union Budget 2023 make the concessional tax regime more lucrative? TOI asks experts to decode the math and also analyze what other steps FM Nirmala Sitharaman can take for taxpayers.

New Income Tax Regime: Existing Tax slabs

The alternate income tax regime was introduced in FY 2020-21 by FM Nirmala Sitharaman. It is subject to certain conditions – mainly disallowance of various deductions). The income tax slabs under this new alternate income tax regime are as under:

To further incentivize individuals to opt for this new optional tax regime, Budget 2023 may look at enhancing the basic tax exemption limit. This will increase the net disposable incomes and hence the spending/ investment capacity of individuals.

Union Budget 2023: Proposed New Income Tax Slabs Under Alternate Tax Regime

Surabhi Marwah, Tax Partner – People Advisory Services at EY India is of the view that increasing the basic exemption limit will lower the effective tax rate. “It does seem to appear that the adoption of the concessional tax regime has been low amongst individual taxpayers,” she tells TOI. “An increase in the basic tax exemption limit to Rs 5 lakh will lower the effective tax rates for individual taxpayers,” she says.

Also Read | Union Budget 2023: Why income tax slabs need to be revised

However, Marwah also advocates introduction of certain exemptions in the concessional tax regime to make it more lucrative for individual taxpayers. According to her, the following exemptions must be considered in the alternate tax regime apart from an increase in the basic exemption limit:

1. Standard deduction should be retained at Rs 50,000

2. Benefit of the section 80C/CCC/CCD/D deduction up to Rs 2,50,000 should be provided. The benefits for these sections should be limited to provident fund including PPF, qualifying life insurance products, interest on housing loan, pension policies, employees/self-contribution to New Pension Scheme and mediclaim insurance.

Parizad Sirwalla, Partner at KPMG in India points out that increasing the basic exemption limit under new tax regime to Rs 500,000 will not benefit the relatively lower income group. “Currently, the basic exemption limit under both the existing and the optional new tax regime is Rs 250,000. Also, resident individuals having taxable income up to Rs 500,000 are not effectively required to pay any tax as they are entitled to a tax rebate of Rs 12,500 or equal to the amount of tax payable (whichever is lower) under both the existing and new regime as well,” she substantiates.

For individuals with income slightly higher than Rs 500,000, the incentive to choose the new alternate income tax regime may be limited. “As an example, if an individual’s gross income was Rs 650,000, he would be neutral to the tax regime selection as he would have still been at NIL tax liability by investing Rs 150,000 in eligible investments under Section 80C of the Income Tax Act, 1961 (the Act),” Sirwalla tells TOI.

For higher income category taxpayers, the quantum of tax benefit under the new optional tax regime would depend on how the tax rate for subsequent income slabs are adjusted. KPMG’s Sirwalla elaborates on tow possible alternatives that the Modi government can consider after increasing the basic exemption limit to Rs 5 lakh.

Also Read | Budget 2023: How new income tax regime can be made more attractive

As alternative 1, post this recommended increase of basic exemption limit (to Rs 500,000), the tax rate of 10% could continue to apply for income between Rs 500,000 and Rs 750,000 and so on and so forth. In other words, there will be no income slab to which the 5% rate will apply. Hence, the tax slabs under the new tax regime would be as under:

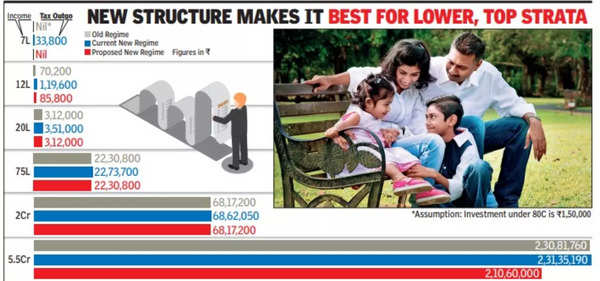

In such a scenario, the below might be the proposed impact/ income tax savings on a per annum (p.a.) basis for an individual, basis the applicable taxable income:

- For a taxable income of Rs 750,000 the income tax savings would be approximately Rs 13,000.

- For a taxable income of Rs 2,000,000 the income tax savings would be approximately Rs 13,000

- For a taxable income of Rs 6,000,000 the income tax savings would be approximately Rs 14,300;

- For a taxable income of Rs 11,000,000 the income tax savings would be approximately Rs 14,950

- For a taxable income of Rs 22,000,000 the income tax savings would be approximately Rs 16,250.

- For a taxable income of Rs 55,000,000 the income tax savings would be approximately Rs 17,810.

Hence, as you will observe the tax savings under this alternative will range from Rs 13,000 p.a. to Rs 17,810 p.a. (base tax of Rs 12,500 plus applicable cess and surcharge).

Also Read | Budget 2023: How income tax burden of common man can be reduced; top 3 ways

As alternative 2, the rate of tax pertaining to each set of taxable income could also be decreased. i.e., post the recommended increase of basic exemption limit (to Rs 500,000), the 5% tax rate could be made applicable for taxable income between Rs 500,000 to Rs 750,000. Considering the same, the threshold limit for the highest tax rate (of 30 per cent) may be increased from 1,500,000 to 1,750,000 consequently.

Hence, the tax slabs under the new tax regime would be as under:

In such a scenario, the below might be the proposed impact/ income tax savings on a per annum (p.a.) basis for an individual, basis the applicable taxable income:

- For a taxable income of Rs 750,000 the income tax savings would be approximately Rs 26,000.

- For a taxable income of Rs 2,000,000 the income tax savings would be approximately Rs 78,000.

- For a taxable income of Rs 6,000,000 the income tax savings would be approximately Rs 85,800.

- For a taxable income of Rs 11,000,000 the income tax savings would be approximately Rs 89,700.

- For a taxable income of Rs 22,000,000 the income tax savings would be approximately Rs 97.500.

- For a taxable income of Rs 55,000,000 the income tax savings would be approximately Rs 1,06,860.

While the tax savings range cannot be determined under this alternative, the maximum tax savings under this alternative 2 can be Rs 1,06,860 p.a. (base tax of Rs 75,000 plus applicable cess and surcharge).

Sirwalla concludes that a careful evaluation will need to be done of various factors by FM Sitharaman before considering an increase in basic exemption limit under the new alternate income tax regime. Some of these factors are number of taxpayers falling out of the mandatory return filing requirement, benefit to common man, net tax collection foregone by the government etc.