[ad_1]

With Union Finance minister Nirmala Sitharaman’s budget announcements coming into force in the new financial year beginning April 1, it is time for salaried individuals to choose between the Old Tax Regime (with exemptions and deductions) and the New Tax Regime, which was made more attractive in the February budget.

As companies will start deducting monthly taxes from salaries beginning this month, employees are required to inform their employers if they want to stay in the OTR or switch to the NTR.

What was announced in the budget?

While Sitharaman did not announce any change in the OTR, under the new system, tax rebate limit was increased to Rs 7 lakh per year from the earlier Rs 5 lakh. This means that people with a taxable income of up to Rs 7 lakh are not required to pay any tax. However, if the taxable income is more than Rs 7 lakh, tax will have to be paid as per the applicable slabs under the new regime.

The government also extended the benefit of standard deduction of Rs 50,000 to taxpayers under the NTR. Till the financial year ending March 2023, this deduction was available only to taxpayers under the OTR.

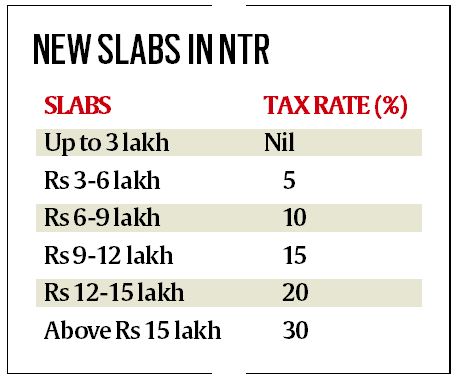

The government announced changes in income slabs and tax rate in the NTR. While tax slabs were redcued from seven to six, the 25 per cent tax rate applicable on income falling between Rs 12.5 lakh to Rs 15 lakh till last year was removed (see table for new tax slabs under NTR).

On the higher end of the spectrum (those with annual taxable income of over Rs 5 crore), the government announced a cut income tax surcharge to 25 per cent from 37 per cent under the new regime. This would reduce the effective rate of income tax for this group from 42.7 per cent to 39 per cent.

In her budget speech, Sitharaman said, “Each salaried person with an income of 15.5 lakh or more will thus stand to benefit by Rs 52,500.” So, while taxpayers under the new tax regime will benefit from this tweaking in slabs and rates and standard deduction (to a maximum of Rs 52,500), the announcement has also made taxpayers under OTR do the math to understand what is better for them.

Should you go for NTR or stay with OTR?

For those with taxable income of up to Rs 7 lakh, the NTR is the obvious choice as they won’t have to pay any tax. For others, there are no clear answers, and the decision depends on the tax slab one falls into and the deductions one claims. It is important to note that the benefits under the old tax regime will be meaningful for individuals only if they manage to claim most of the deductions available.

Analysis across various tax categories with various deduction claims shows that individuals with gross taxable income of up to Rs 10 lakh and claiming all deductions will benefit the most from the old regime. The benefits tend to decline for higher incomes, as under the OTR, income above Rs 10 lakh is taxed at 30 per cent, whereas in the NTR, income between Rs 10 lakh and Rs 12 lakh is taxed at 15 per cent and that between 12 lakh and Rs 15 lakh is taxed at 20 per cent.

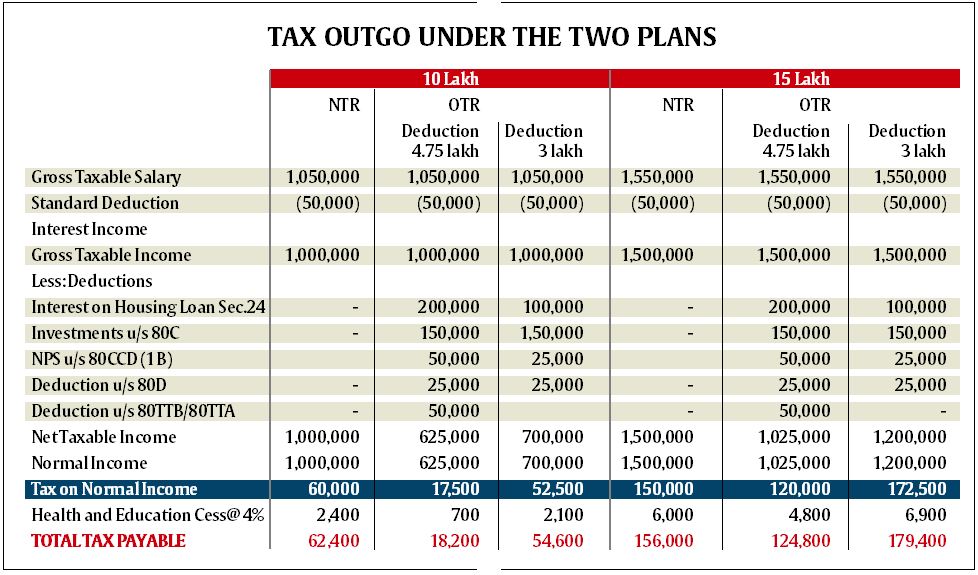

What happens if your gross taxable income is Rs 10 lakh?

Analysis shows that those with a gross taxable income of Rs 10 lakh would pay a tax of Rs 62,400 under the new tax regime. In the OTR, if they claim the maximum of all the five deductions (aggregating to Rs 4.75 lakh), under the heads of interest payment on home loan (Rs 2 lakh); EPF/ PPF/ life insurance/ ELSS etc. under Section 80C (Rs 1.5 lakh); NPS under Section 80CCD (Rs 50,000); health Insurance for self (Rs 25,000) and health insurance for parents (Rs 50,000), they would pay tax amounting to only Rs 18,200 and thus save Rs 44,200 per annum over what they would pay under NTR.

However, if they claim deductions amounting to only Rs 3 lakh, the difference of benefits under OTR declines to Rs 7,800. Further, if they only claim deductions of Rs 2.5 lakh in a year, then under OTR, they would end up paying a total tax of Rs 65,000, which is Rs 2,600 more than under NTR.

What happens if your gross taxable income is Rs 15 lakh?

For those with gross taxable income of Rs 15 lakh, under the NTR, the tax outgo would amount to Rs 1,56,000. Under OTR, if they claim all the deductions, amounting to Rs 4.75 lakh, they would pay a tax of Rs 1,24,800 and save around Rs 31,200 per annum. However, if they claim deductions amounting to Rs 3.75 lakh, then under OTR, they would pay the same tax as under NTR, i.e Rs 1.56 lakh.

In case they claim deductions amounting to only Rs 3 lakh, they would end up paying a tax of Rs 1,79,400 under the OTR, thereby paying an additional tax of Rs 23,400 over that in NTR. For income above Rs 15 lakh, there is no difference between NTR and OTR as far as tax rates are concerned, as taxable income above Rs 15 lakh attracts a 30 per cent tax rate in both the regimes.

As the above analysis shows, the final call between OTR and NTR will depend upon how much deduction one claims and in what tax bracket one falls. Individuals need to consult their financial advisor or tax consultant to arrive at the right decision.

[ad_2]

Source link

For more information call us at 9891563359.

We are a group of best insurance advisors in Delhi. We are experts in LIC and have received number of awards.

If you are near Delhi or Rohini or Pitampura Contact Us Here